之前说的塔勒布关于比特币的论述多少有点隔靴搔痒,因为推特也都只是只言片语,要理解他完整的意思不可避免的还是要回到他那个论文《Bitcoin, Currencies, and Fragility》。这文章很长,我时间精力有限,粗糙的翻译一下。因为里面涉及到不少专业内容,我会写点注释和导读。到一个阶段的最末尾,我才会说我自己的看法。

体例:

英语是论文原文,包含标题和段落分割

[1]是论文原文里的对其他论文的引用

(*)是笔者的附加说明和评述

2这类右上角的标注表示论文里的注释

论文里引述其他论文的部分使用引用的格式

Bitcoin, Currencies, and Fragility

比特币,货币及其脆弱性

A technology should be judged in how it solves recognized problems, not by its technical appeal.

一种技术的价值应该取决于它解决特定问题的作用,而不是它的技术有多厉害。

INTRODUCTION/ABSTRACT

综述

This discussion applies quantitative finance methods and economic arguments to cryptocurrencies in general and bitcoin in particular —as there are about 10, 000 cryptocurrencies, we focus (unless otherwise specified) on the most discussed crypto of those that claim to hew to the original protocol [1] and the one with, by far, the largest market capitalization.

本文将把量化金融的办法和经济学方法应用于加密货币,特别是比特币——由于加密货币约有10000种,我们将重点(除非另有说明)关注最被广泛讨论的,创世的第一种加密货币[1],也是市值最大的一种加密货币。

In its current version, in spite of the hype, bitcoin failed to satisfy the notion of “currency without government” (it proved to not even be a currency at all), can be neither a short nor long term store of value (its expected value is no higher than 0), cannot operate as a reliable inflation hedge, and, worst of all, does not constitute, not even remotely, a safe haven for one’s investments, a shield against government tyranny, or a tail protection vehicle for catastrophic episodes.

就当下而言,尽管不断有人大肆鼓吹,但比特币也并未能实现「无需政府的货币」的构想(事实证明,比特币甚至算不上是一种货币),既不能作为短期或长期的价值储存(其价值甚至不比0高),也不能作为可靠的通胀对冲工具。最糟糕的是,长期来看比特币也没办法用来对抗货币当局的滥发,也不能为灾难性的尾部事件充当对冲保护的工具。

(*)尾部事件是指发生概率很小的,在分布函数尾部的事件,可粗略理解成小概率事件。

Furthermore, bitcoin promoters appear to conflate the success of a payment mechanism (as a decentralized mode of exchange), which so far has failed, with the speculative variations in the price of a zero-sum maximally fragile asset with massive negative externalities

另外,比特币的推广者们似乎想要融合投机属性和支付属性(一种去中心化的交易方式),尽管把比特币做为支付工具已经失败,依然试图调和比特币支付属性与零和博弈的投机属性。而这个用于零和投机游戏的脆弱资产,带来了巨大的负外部性。

(*)负外部性是经济学术语,可以粗略的理解为对社会有害

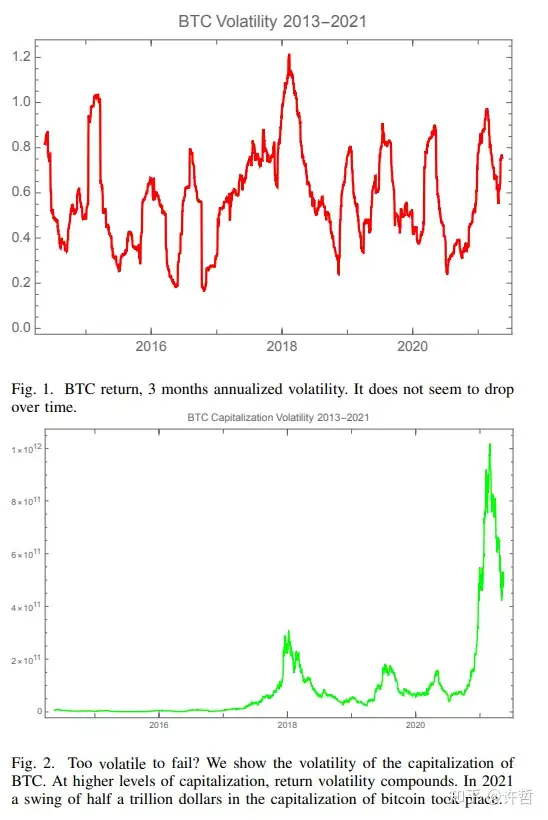

(*)该图是比特币价格波动率的一个统计,波动率通常是描述资产价格不稳定性的指标,用价格变化的方差来刻画。波动率大意味着作为支付工具是不可用的。

Going through monetary history, we show how a true numeraire must be one of minimum variance with respect to an arbitrary basket of goods and services, how gold and silver lost their inflation hedge status during the Hunt brothers squeeze in the late 1970s and what would be required from a true inflation hedged store of value.

纵观货币历史,我们展示了一个真正的基准货币,应该对任意一揽子商品和服务满足最小方差。以及黄金和白银如何在1970年代后期亨特兄弟的操纵案后失去了通胀对冲地位,然后讨论如何能真正对冲通胀,保持价值。

THE BLOCKCHAIN

区块链

First, let us consider what cryptocurrencies do by examining the notion of blockchain and its intellectual and mathematical appeal.

首先,我们来研究一下加密数字货币用什么办法来验证,区块链它背后的机制和数学方法。

(*)关于比特币原理的简介,网上有很多,这里说的实在是不够清晰,强烈推荐 3blue1brown 比特币原理简介;了解了比特币的原理后关于原理部分的描述可以扫一眼跳着看

The concept behind such a chain is quite intuitive to early practitioners of quantitative finance. Consider that before efficient software for Monte Carlo simulations became widely available, some of us were using methods to generate pseudorandom variables via some forms of chained nonlinear transformations, in the spirit of Von Neumann’s original idea [2].

对于链背后的概念,对于早期量化金融的参与者们来说都是老熟人了。在蒙特卡洛模拟软件被普及之前,我们经常用链式非线性变换的方法来生成一个伪随机变量,这个也是冯诺依曼最初想法的精神[文献2]。

Indexing sequences by �=1,2,…� , with a seed at � , a variable �� on the real line generates via nonlinear transformations �:�→� , an output variable �(��) . This output variable can serve as a pseudorandom seed to generate another pseudorandom variable, �(��+1) . For all � , knowledge of �(��) allows knowledge of all subsequent variables �(��)τ>� and replication of the entire sequence, thus probabilistically mimicking the arrow of time. It is also crucial that the same seed produces exactly the same pseudorandom variable, allowing verification of sequence, but disallowing easy reverse engineering.

(*)如果你看着头晕,确保你知道哈希函数是什么的情况下可以跳过,如果还不知道,但能看点简单的代码,推荐参考 关于哈希算法

一个有序的序列 �=1,2,…� 上取一个种子 � ,一个变量 �� 在实数轴上做一个非线性的变化 �:�→� , 生成一个输出变量 �(��) .这个输出的变量可以用来作为一个伪随机种子来生成另外一个伪随机变量 �(��+1) .

对于所有 � , 已知的 �(��) 可以推导出后续的变量 �(��)τ>� 以推导出整个序列,从而构造出一个时间上的箭头来。至关重要的是,同样的种子能产生完全相同的伪随机变量,是便于验证的,但没法进行逆向工程。

What the blockchain added, thanks to the hash function, is the condition that �(.) must be functionally and probabilistically bijective: no two seeds should produce the same output (or should produce a vanishingly low probability of that happening), what, in computer science terminology, is called collision.

感谢哈希函数的特性,区块链增加了一个特性,在 �(.) 在功能和概率上都必须满足双射(bijective)的条件下:没有两个不同的种子能产生一个相同的结果(或者在概率上几乎不可能),在计算机科学的术语里,这种情况成为冲突(collision)。

(*)如果你知道哈希函数是啥,可以直接跳过。不知道的再看一遍 关于哈希算法

This hard-wired attribute and absence of supervision of the blockchain allow the storage of activities on a public ledger to facilitate peer-to-peer commerce, transactions, and settlements. The blockchain concept also allows for serial record keeping. This is supposed to help create what the original white paper [1] described as:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.

因为这个哈希函数的固有性质和监管的缺失区块链技术能让大量的活动记录在一个公共的账本上,使得一个纯「点对点」的网络能记录商业活动,支付和清算。区块链的概念还能对连续的记录做到不可篡改的保存。这些性质为了实现中本聪白皮书描绘的目标:

一个纯的点对点版本的电子现金,可以让在线支付从一方直接支付到另外一方,而不依赖任何中间金融机构

From that paper, bitcoin makes use of three existing technologies: 1) the hash function, 2) the Merkle tree (to chain blocks of transactions tagged by the hash function), and 3) the concept of proof of work (used to deter spam by forcing agents to use computer time in order to qualify for a transaction) — technologies that, ironically, all came out of the academic literature[3]1 . The idea provides a game theoretic approach to mitigate the effects of the absence of custodian and lack of trust between participants in the maintenance of a permanent shared public ledger — attenuating or circumventing the coordination quandary known as the “Byzantine general problem”.

在中本聪的这篇论文里,比特币使用了三项已经存在的技术:1)哈希函数,2)默克尔树(把一个个由哈希标记的记录数据块链接起来),和3)POW的概念(曾经用来阻止垃圾邮件的一个办法让计算机的工作时长来验证方法)。讽刺的是,所有这些技术都并不新,都是学术界早已有之的文献里[3] 1 。这个主意(指区块链技术)提供了一种博弈论层面上的方法,以缓解在维护永久公共账簿时缺乏托管人和参与者之间缺乏信任的问题。减弱或者绕过一种名叫「拜占庭将军问题」的协调困境。

(*)使用已经成熟很久的技术拼凑出一个新技术并不丢人和讽刺,利用久经考验的技术会让技术更可靠,这并没问题。显得略有讽刺是区块链技术的鼓吹者把这项技术吹得过于跨时代,好似再造天地一般。这个锅是区块链的过度鼓吹者的,笔者并不认为这是区块链应该被诟病的点。

1 As this discussion is focused on proof of work, we exclude from it Ethereum and other cryptocurrencies.

1 这里专注在讨论纯POW上,我们排斥类似以太坊或者其他加密数字货币

(*)以太坊要转用POS等完全原理上不同于POW的技术,之后关于POW的论述均不适用

The bitcoin transactional currency (BTC) system establishes an adversarial collaboration between the so-called “miners” who validate transactions by getting them on a public ledger; as a reward they get coins plus a fee from the underlying transactions, transfers of coins between parties. The proof of work method has an adjustable degree of difficulty based on the speed of blocks, which aims, in theory, to keep the incentive sufficiently high for miners to keep operating the system. Such adjustments lead to an exponential increase in computer power requirements, making at the time of writing onerous energy demands on the system — energy that could find alternatives in other computational and scientific uses.

比特币系统的可交易货币(BTC)建立在「矿工」们的竞争性合作上,矿工的责任是去验证公共账本上的交易是否合法;矿工会在验证参与者之间交易合法性的过程里获得一些币作为奖励。POW的算法会根据出块的速度来调整挖矿难度,理论上这个设计旨在为矿工创造足够的激励以保证网络的安全。这种调整造成了计算机算力需求指数性的增长,这需要能源的保证。这些算力和能源完全是可以用来做其他可算和科研用途的。

Miners derive their compensation from both seignorage (the market value of a bitcoin minus its mining costs) and transaction fees upon validation — with the plan to switch to transaction fees as the sole revenues upon the eventual depletion of the coins, which are limited to a fixed number.

A central attribute is that bitcoin depends on the existence of such miners for perpetuity.

Note that the entire ideological basis behind bitcoin is complete distrust of other operators — there are no partial custodians; the system is fully distributed, though prone to concentration 2 . Furthermore, by the very nature of the blockchain, transactions are irreversible, no matter the reason.

矿工们有两个收入来源,一为铸币税(比特币的市值减去挖矿成本)和交易验证的手续费,这个手续费是计划在所有的挖矿奖励耗尽之后作为所有的收入,最后收敛在一个固定的数字。

(*)这里是比特币区块奖励的机制,每过一段时间区块奖励减半,最后直到没有,从而保证比特币的总量上限存在一个固定数字。当比特币达到最大值时,矿工的所有收益均来自于手续费。

比特币系统的存在完全是依赖于矿工们永久参与。

(*)意思是当区块奖励消失后,矿工们能否继续参与挖矿有问题,但比特币唯一的物理存在就是矿工,矿工要是不干了就彻底废了。这个担忧是确实存在的,矿工圈内亦有激烈讨论,不是空穴来风。

注意一下比特币背后的整个意识形态是对任何运营商性质的东西彻头彻尾的不信任,这里没有任何托管的概念;整个体系是彻底分布式的,虽然比特币有强烈的集中化的倾向 2 。还有,比特币无论如何交易是不能逆转的,无论什么原因它就是不能。

2From public data, we were able to verify that the distribution of holdings of bitcoin follows a powerlaw with tail index ≈54 , no different from the distribution of wealth in the U.S.

2从公开数据上来看比特币的持有者符合幂律分布,集中度非常之高,和美国的财富分布程度差不多。

(*)意思是比特币是集中在少数人手上的,所以理念上的去中心化并没什么卵用,还是掌握在几个中心手上

Finally, note that bitcoins are zero-sum by virtue of the numerus clausus.

最后,注意一下比特币是一个零和游戏在一个numerus clausus 数里不断转手而已。

(*)这里的numerus clausus 是拉丁语,意思是「closed number」,意思是比特币就在一个封闭的小圈子里互相搞一个零和的游戏而已。四个人打麻将永远创造不出价值的。

As we will see, mathematical and combinatorial qualities do not necessarily translate into financial benefits at either individual or systemic levels.

所以我们可以看到,数学的各种组合性质并不一定能转换成各种真实的经济价值,无论是对个体而言还是对整个经济体系而言。

Comment 1: Why BTC is worth exactly 0

Gold and other precious metals are largely maintenance free, do not degrade over an historical horizon, and do not require maintenance to refresh their physical properties over time. Cryptocurrencies require a sustained amount of interest in them.

评论1:为什么比特币的价值就是0

黄金和其他贵金属是不用花钱来维持的,它们不会随着时间的流逝而降解,因为它们的物理属性决定了他们不需要主动维护。而加密数字货币需要持续不断的利益去让人们维系它们的存在。

VULNERABILITY OF REVENUE-FREE BUBBLES

无收益资产泡沫的弱点

A central result (even principle) in the rational expectations and securities pricing literature is that, thanks to the law of iterated expectations, if we expect now that we will expect the price to vary at some point in the future, then by backward induction such a variation must be incorporated in the price now. When there are no dividends, as with growth companies, there is still an expectation of future earnings, and a future expected reward to stockholders — directly via dividends, or indirectly via reverse dilutions and buybacks. It remains that a stock is a claim on accumulated assets and their residual value.

在一个理性期望的情况下(哪怕只是原则上的)或者是证券定价原理所阐述的那样,幸好我们有「双重期望值定律」,如果我们现在预期未来某个点我们会有一个对价格的期望,那么通过反推演算,这种变数一定包含在当下的价格之中。就算是没有股息的成长股也是对未来的收益有一定的期望,这个期望是指对股东在未来的回馈——无论是直接现金股息分红,或者是非直接的反稀释和回购等形式。股票仍然是对累积资产及其剩余价值的索取权。

(*)这里讲的未来贴现的股票定价模型,可以参考:如何简单明了地解释自由现金流折现?

(*)这里的范围要略广一些,不仅仅是股息回报,所有的回购增加股东权益的行为都囊括进去了,意思是说明一个资产必然是因为未来有回报的(无论是不是以现金分红的形式)才造就了它当下的「贴现价值」。

(*)并且未来在某个条件下产生的某种期望的综合效果,和当下无视未来事件对期望的影响也一定是相同的,双重期望值定律给我们估值带来的巨大方便。

(*)双重期望值定律: �(�)=�(�(�|�))

(*)当Y条件下X的期望值,也就是未来股票或者资产产生某些事件对我们估值的影响(利好或者利空的事件),长期综合考虑它们影响的总和,也就是对所有条件期望再求期望,和无条件期望(完全不考虑未来可能产生的利多利空,也就是无视条件概率事件)最后必然也是一致的。

(*)我再换人话一下:风风雨雨最后长期还是看内在,当下只要观察长期价值,当下也必然反应长期。因为有双重期望值定律,我们不需要考虑太多可能产生条件下期望的事情对当下估值的影响,使得资产估值变为可能。

(*)再透一点,价值投资可以彻底无视未来可能对价值预估产生变动的扰动,因为这些未来潜在的扰动其实也已经含在现在都价格里。因为未来是不可知的,所以有了双重期望值定律,我们才有可能定价,无惧未知。

(*)这些都是为了说明价值投资理论的内涵用于后续的论述。

Earnings-free assets with no residual value are problematic.

The implication is that, owing to the absence of any explicit yield benefitting the holder of bitcoin, if we expect that at any point in the future the value will be zero when miners are extinct, the technology becomes obsolete, or future generations get into other such “assets” and bitcoin loses its appeal for them, then the value must be zero now 3 .

无收益资产是很成问题的。换言之,因为比特币的持有者是没有明确的期望收益。如果我们知道在未来的任意某一个时刻比特币的价值为0,比如矿工最后因为没区块奖励不干了,技术被更新换代了,或者新时代炒作的主题变成了其他「资产」比特币失去了投机的关注度,那么比特币现在的价值就应该是零3。

(*)在价值投资里,一个东西未来的价格如果是0的话,那么它的「现值」必然是0。

(*)这段话的意思是比特币作为一个必须要有「后来人」接盘的东西,本身是无收益资产的话,那么几个可能让比特币归零的可能性存在,比特币的现值就应该是0。

(*)肯定有人会说黄金白银也是无收益资产,不照样不归零还新高嘛,这个在后文里有讲到。我们先来看小注释3的内容

3Using a traditional rational bubble model (see [4] and the review by [5]), we get the following conditions. Let �� be a discount rate and � be a probability of absorption over a period. To escape the barrier, bitcoin must grow at ��+� forever, but no more, without remission, and with total certainty.Should it grow then stabilize, it still would be prone to extinction. We note that traditionally, models rule out any continuous growth at an exponential rate faster than �+� because the security or asset would then represent the entire economy. Bitcoin distinguishes itself from other assets because of its fragility as a mere book entry on a virtual ledger that requires constant refreshing ad infinitum.

3用一个传统的泡沫模型(参考文献[4]和文献[5]),我们需要满足如下的条件,令 �� 为贴现率并且令 � 作为一个周期内的逃逸速度的概率。如果要逃离泡沫崩盘,比特币必须永远以 ��+� 的速度上涨才能逃逸,且不能有任何一丝丝衰退,且100%肯定在增长。就算它稳住在一个水平,它也会有毁灭的倾向。我们注意到传统的这个泡沫模型排斥力任何连续增长速度快于 �+� 的情况因为证券或者资产是反应经济的。而比特币完全把自己排除在这之外,因为它仅仅是一个公共账本里的一个值,是很脆弱的,必须无穷无尽的增长。

(*)这两篇关于泡沫模型的论文我没读过,不过看着似乎挺有意思的。塔勒布的意思是根据这个泡沫模型,一个靠后来者接盘的东西本质上是一个旁氏模型,然后必须维持一定的增速,否则旁氏骗局就崩盘了。具体的推导过程大家可以去看引述的原论文。所有引述的论文最后会罗列。

(*)一个旁氏盘子必须药不能停,这个是肯定没问题的。如果比特币是完全依赖后来者以更高价格买走的旁氏的话,那么它维系存在的增长需求也是不断增长直到不可能的。塔勒布大致的意思是比特币那是比一般泡沫要虚得多的泡沫里的战斗机。

The typical comparison of bitcoin to gold is lacking in elementary financial rigor 4 . We will see below how precious metals lost their quality as a medium of exchange; gold and other dividend-free precious items (such as other metals or stones) have held some financial status for more than 6, 000 years, and their physical status for several orders of magnitude longer (i.e., they did not degrade or mutate into some other alloy or mineral). So one can expect one’s gold or silver possessions to be around physically for at least the next millennium, as well as having some residual economic value by iteration, for the same reason. Metals have ample industrial uses with demand elasticity (and substitution for other raw materials). Currently, about half of gold production goes to jewelry (for which there are often no storage costs), one tenth to industry, and a quarter to central bank reserves.

经常拿黄金和比特币作比较这个是在金融问题上一个很幼稚的错误 4 。我们下面会看到贵金属是怎么失去它们的交易媒介属性的;黄金和其他非生息的贵重物(比如其他的金属或宝石)的金融属性有保持了超过6000多年,他们的物理属性能保持超过这个时间好几个数量级(他们不会衰变或者降解成其他物质)。所以我们能期望自己的黄金或者白银财产至少在下一个千年依然保持相同的物质形态,并且还有一些残存的经济价值。金属还会有很多工业价值,且有需求弹性(由其他金属的替代效应)。目前,黄金的产量一半用于珠宝业(一般这个行业不会有折旧损耗),十分之一用于工业,四分之一用于央行储备。

(*)意思是说贵金属宝石啥的并不是啥天然的货币,6000多年的金融属性历史远比不上它们更久远的历史,贵金属宝石等作为货币只占它们历史的很小一段,而且现在贵金属也失去了货币属性了。所以不存在什么金属天然是货币。且金属这类非生息资产因为有工业属性和其他用途,比如就是人们纯粹喜欢黄金而有价值。

(*)为什么把比特币称为电子黄金是不对的,是注释4的内容。

4 It is also a reasoning error to claim that an innovation, bitcoin, can become the “new gold” ab ovo, when gold wasn’t decided to be so by fiat thanks to a white paper; it organically became a reserve asset ex post, through centuries of competitive selection against other modes of storage, payment, and collectibles. Gold elicited an aesthetic fascination and had been used as jewelry and store of value for more than two millennia before it became, literally, a currency or before there was such a thing as a currency. The Phoenicians used it as store of value because there was demand for it, and it was not until the 6 th C. BCE that coins from Sardis became a widespread means of exchange [6].

注释4:声称比特币是一个伟大的创新因为它变成了一个「新黄金」从一开始就是一个归因错误。当黄金还没有成为那么「法币」的时候,它很早就成为了一个储备资产了,在过去很多世纪里它和不同形式的存储物支付工具和收藏品竞争。黄金引领了一种审美被用于珠宝和价值存储是要远早于它变成字面意义上的货币至少两千年。腓尼基人用它作为存储价值的工具是因为他们很渴望黄金,直到公元前6世纪,萨迪斯的硬币才成为一种广泛的交易手段[6]。

(*)这段注释的意思是不能倒果为因,黄金在成为货币前因为大家都很想要了,所以才脱颖而出变成一种储备资产,然后才有把黄金当做货币的事情发生。是先有大家想要黄金为因,才有黄金被当做货币为果。先宣传一个东西是货币,然后说它是新黄金是不对的。

(*)一个东西能成为货币储备是因为大家想要它,而不是它像黄金。黄金也是因为大家要它,它才成为货币储备资产的,而非反过来。

(*)到这里大致的意思是要么一个资产是生息资产,我们能通过贴现模型的方式估值资产。而一个纯粹靠后来者接盘维系价格的旁氏结构未来对增长的需求会达到不可能实现而必然走向崩盘。比特币是非生息资产。

(*)例如黄金这样的也是非生息资产的东西,它能保持自己的价值是因为有需求,或者珠宝业人家喜欢黄金,或者是工业属性。且黄金存在的时间远远长于其作为货币属性的时间。是因为黄金被广泛的有需求了,才会让黄金脱颖而出成为货币的一种候选,并且黄金现在也失去了货币属性。

(*)所以因为比特币和黄金一样是稀缺不可再生的,就论证比特币一定会像黄金一样具备货币属性(黄金自己都没有了),这个逻辑推断是不成立的。是先有需求才有储备价值,才发展成货币。而非单纯因为稀有。如果比特币不能让人产生需求,仅就不可再生和稀缺的话,是站不住脚的论断。

(*)要么你拿贴现模型来,要么有人消费的供需模型来,否则就得用泡沫模型了,是个泡沫迟早要灭。如果迟早要灭,那么贴现价值也就是0了。

Path dependence is a problem. We cannot expect a book entry on a ledger that requires active maintenance by interested and incentivized people to keep its physical presence, a condition for monetary value, for any period of time — and of course we are not sure of the interests, mindsets, and preferences of future generations.

Once bitcoin drops below a certain threshold, it may hit an absorbing barrier and stays at 0 — gold on the other hand is not path dependent in its physical properties 5 . As discussed in [7], technologies tend to be supplanted by other technologies with a vulnerability in proportion to their past survival duration (>99% of the new is replaced by something newer), whereas items such as gold and silver have proved resistant to extinction.

路径依赖也是一个问题。我们不能指望区块链的账本信息一直考对比特币有兴趣的参与者们长期维护其物理存在,从而保留起货币价值,未来任意一个时刻没人维护了就都不存在了。并且我们肯定是没法确定未来世代的人的想法兴趣和行为方式。

一旦比特币的价格跌到一定的临界值,那个它将会撞上一个「吸收壁」,并且保持价格为0,黄金恰恰相反,它不依赖其他的维系方式能独立保持其物理属性。如[文献7]里讨论的一样,技术往往会被其他技术所取代,这些技术的弱点与其过去的生存时间成正比(>99%的新生事物会被更新的食物取代)。而金银等物被证明是会长期保持不灭的。

(*)意思是比特币和黄金白银不一样,它要维持自己在物理世界的存在,需要矿工们持续支付代价来维持存在。而未来的人是不是会继续对比特币网络有那么高的兴趣来维护昂贵的区块链的运行成本,我们没办法知道。如果有更好的记账技术了,比特币主链会被放弃,那就会归零,而未来会归零的东西的贴现值就是零。也就是说除非币圈信仰充值药不能停能维持到天荒地老,并且当中不能有任何断档,不然迟早有一天要归零。中间任何一个10分钟都不能断是颇为脆弱的。

(*)长期来看,很难想象比特币的区块链技术就是最优版本,这也不符合计算机软件发展的规律。目前比特币的主链是否会是未来的最大市值链,甚至是否有挖矿的经济效益,确实是不确定的。并且未来如果有比区块链更好的作为记账的手段,抛弃区块链也不是不可能的事情。但这个未来可能会有更好方案的推论其实可以普适于一切对技术的评论。笔者认为这种诘难过于宽泛。

(*)但区块链需要一刻不停的以高成本维护确实是一个脆弱点,触及「吸收壁」效应的话,可能就会发生比较大的问题。相比于贵金属等而言需要高维护成本是一个实打实的弱点和劣势,这是不可否认的。下面的注释 5 会进一步解释「吸收壁」效应。

(*)硬分叉或许是一个保持动态升级的办法,虽然其有负面效应,一刻不能停确实是一个很严苛的要求,很难想象长期到千年的级别,区块链能保持 always online。笔者更加相信在链在技术上撞到脆弱性的时间要晚于有比目前区块链技术更好的新技术的出现的时间。比区块链更优的新技术让挖矿成为不经济行为的可能性更大。

5 The absorbing barrier does not have to be 0 for the price to spiral to 0 upon hitting the barrier. This is similar to saying “if the heart rate drops below ten beats per minutes, it will be 0 (death)” — nor does it necessarily have to be caused by a drop in price.

5吸收壁并不一定需要归零后才会触发死亡螺旋。这个有点类似说「如果心率降低到每分钟十次的话,心率迟早是要归零的(死亡)」——这个归零也不一定是需要由价格归零触发点。

(*)吸收壁效应的意思就是临界触发死亡螺旋的这么一个比喻,一旦触及到了,就不可逆的走向灭亡。

Furthermore bitcoin is supposed to be hacker-proof and is based on total infallibility in the future, not just at present. It is crucial that bitcoin is based on perfect immortality; unlike conventional assets, the slightest mortality rate puts its value at 0 6 .

另外比特币被认为是被黑客攻击久经考验下来非常安全的资产,并且未来会一直安全,不仅仅是现在安全。比特币在安全性上的完美无瑕对于比特币来说是至关重要的。不像传统资产,略有一丝的瑕疵就会要了比特币的命。

(*)从信息安全的角度上来说,没有绝对安全的系统,比特币亦然。比特币的区块链技术在历史上也有几次安全漏洞和更新,但并不是所有的安全漏洞都触发了吸收壁。但这确实是一个很大的风险隐患,我们确实没法确定比特币是否目前还藏着致命的安全性缺陷,没人知道。相比于黄金这类靠物理定律保持稳定的,确实是个劣势。而一旦有概率不小于0的比特币漏洞能导致比特币网络出致命问题,那么它的贴现值就是0这个推论是正确的。由此可以构造同义的句子:在未来无穷长的时间内,比特币技术存在任意致命漏洞的概率大于0的情况下,比特币当下的贴现价值为0。比特币:我太难了……

6 To counter the effect of the absorbing barrier, the asset must grow at an exponential rate forever, without remission, and with total certainty. Belief in such an immortality for BTC — and its total infallibility — is in line with the common observation that its enthusiastic investors have the attributes of a religious cult.

6要对抗吸收壁效应的话,资产段增值必须以一种指数爆炸的性质永远增长,并且不能有衰退,且完全肯定。对于比特币完全不朽的信念,和人们观察到的币圈近乎宗教信仰式的热情是完全一致的。

(*)意思是比特币泡沫不触及到吸收壁除非有宗教信仰般的热情,否则不可能。而现在比特币还杵在那里是因为我们确实看到币圈搞的跟邪教一样。

Principle 1: Cumulative ruin

定律1:持续损耗原理

If any non-dividend yielding asset has the tiniest probability of hitting an absorbing barrier (causing its value to become 0), then its present value must be 0.

如果任意一个非生息资产有哪怕再小点概率撞到吸收壁上(能让它归零的),那么它的现值就是0。

(*)上一篇的贴限值理论和链接可以参考阅读,反复在用这个推论。

We exclude collectibles from that category, as they have an aesthetic utility as if one were, in a way, renting them for an expense that maps to a dividend — and thus are no different from perishable consumer goods. The same applies to the jewelry side of gold: my gold necklace may be worth 0 in thirty years, but then I would have been wearing it for six decades.

我们排除了收藏品品类,因为它们具有美学价值,某种意义上来说,租用这些收藏品获取的效用就和收到股息分红是一样的,这和快销易腐食品差不多。同样适用于黄金首饰等。我的大金链子可能在三十年里价格归零,但到那个时候我已经戴了六十年了。

(*)意思是收藏品这类的持续在给人产生消费价值,这个持续产生的消费价值和股息分红是一个意思。是分批「划拨」给持有者的。大金链子戴六十年给塔勒布带来的效用已经「回本」了。

(*)这里得理解经济学上关于「效用」的意思,未必是金钱上的,满足你需求的都能改变人的经济行为。假如你买了一幅画,你越看越舒坦,其美学价值让你吃饭后看个十分钟就能觉得妙不可言,然后你持续看了三十年到你撒手人寰被你儿子贱卖掉。那么这三十年来给的这个舒适感也可以算作是「效用分红」,算变相的派息。

(*)按照这个收藏品效用的算法,NFT比BTC靠谱,我一时略有凌乱。抬个杠,我钱包里有比特币特看着就特满足算不算呢?

The difference between the current bitcoin bubble and past recent ones, such as the dot-com episode spanning the period over 1995-2000, is that shell companies were at least promising some type of future revenue stream. Bitcoin would be allowed to escape a valuation methodology had it proven to be a medium of exchange or satisfied the condition for a numeraire from which other goods could be priced. But currently it is not, as we will see next.

比特币的泡沫和过去几十年的泡沫,比如在1995-2000年的.com互联网泡沫不一样的是,互联网泡沫好歹空壳公司们还承诺未来会以某种形式创造现金流收入。比特币如果想要不用这种估值方式定价的话,则比特币必须被证明一种交易媒介或者其他各种商品的估值模式。但目前来看,并没有,我们下面会论述。

(*)意思是纯交易媒介,也就是现金货币是不能用上面说的那些估值模式来定价的,或者世界上还有一些特殊的资产定价的模式,如果比特币是货币属性的话,就可以超然。塔勒布认为并没有。

SUCCESS IN WRONG PLACES

在错误的领域里成功

More generally, the fundamental flaw and contradiction at the base of most cryptocurrencies is, as we saw, that the originators, miners, and maintainers of the system currently make their money from the inflation of their currencies rather than just from the volume of underlying transactions in them. Hence the total failure of bitcoin to become a currency has been masked by the inflation of the currency value, generating (paper) profits for a large enough number of people to enter the discourse well ahead of its utility.

总的来说,大多数加密数字货币根本性的缺陷和矛盾是:我们看到的,发起者矿工和维系整个体系的参与者们是从通胀里赚钱的,而不是通过他们都货币来清算各种交易从而产生收益的。因此比特币作为货币的尝试是彻底失败的,但这个失败被货币价值的通胀所掩盖,产生了大量的账面盈利,大到足以让人们不关心它作为货币的效用本身。

(*)这里说的是比特币作为货币属性的失败,如果是一个货币那么应该根据利用该货币清算的交易来得出它的媒介价值,也就是 ��=�� ,当使用一个货币清算的商品数量和价格足够多的时候,货币是有价值的。但比特币并没用来清算什么贸易,而是一个通胀里的纸面富贵的游戏而已。

(*)人们沉迷于这个账面盈利的游戏,以至于不关心它有没有真的当货币用,这个是币圈里的现实。之前有尝试过比特币作为支付工具的创业公司,无一例外的都没成功,比特币在交易媒介领域并不成功。最初用比特币买披萨的反而是一个正途,而后期比特币虽然市值很高,但作为货币的尝试是失败的。但是 Who cares,币圈的人都盯着某某某发财了我也想要,比特币是不是货币确实没人关心。

Comment 2: Success for a digital currency

数字货币的成功标准

There is a mistaken conflation between success for a “digital currency”, which requires some stability and usability, and speculative price appreciation.

一个「数字货币」需要成功的话,有一些矛盾:它要求稳定性和可用性,又要求有价格投机的价值。

Transactions in bitcoin are considerably more expensive than wire services or other modes of transfers, or ones in other cryptocurrencies 7 . They are order of magnitudes slower than standard commercial systems used by credit card companies —anecdotally, while you can instantly buy a cup of coffee with your cell phone, you would need to wait ten minutes if you used bitcoin 8 . They cannot compete with African mobile money. 9 . Nor can the system outlined above —as per its very structure —accommodate a large volume of transactions — which is something central for such an ambitious payment system.

比特币的交易转账费用是很贵的,比电汇或者其他形式的转账要贵很多,就算和其他加密数字货币比也很贵。比特币转账要花费很长时间,相比于信用卡公司的系统,你如果要买一杯咖啡的话你可以用手机立刻完成支付,但如果你要用比特币的话,起码要等十分钟以上。甚至比不上非洲的移动支付,更别说和上面提到的其他方式比了。而比特币的结构设计也没办法承载大容量的交易——这对于一个雄心勃勃的支付系统来说应该是核心功能才对。

(*)批评比特币支付手段又慢又贵,比特币每秒7笔的处理速度从开始就被人诟病,大区块路线和闪电网络等方案也都是针对这个问题的。客观的说,原版的比特币作为一个通用支付系统,肯定是不够看的。

7 Transactions in bitcoin are orders of magnitude more expensive than those done using African mobile phones.

比特币的交易费用比非洲移动支付都要贵得多

8 “As it grew in popularity, Bitcoin became cumbersome, slow, and expensive to use. It takes about 10 minutes to validate most transactions using the cryptocurrency and the transaction fee has been at a median of about $20 this year.” By Eswar Prasad, New York Times, Jun 15, 2021.

比特币的交易支付体系又笨重又慢而且很贵,用了10分钟才验证了一笔交易而且这个交易的平均费用高达20美元,Eswar Prasad,纽约时报,2021年6月15报道

9 There appear to be other protocols issued from the original white paper that claim to be more transaction focused; as with Ethereum, we exclude them from this analysis.

这里讨论的是原版白皮书的比特币协议,其他一些协议号称要专注在交易速度上,比如以太坊,我们这里不讨论那一些

(*)蛤?这是没见识过以太坊大堵塞吗?!

To date, twelve years into its life, in spite of all the fanfare, but with the possible exception of the price tag of Salvadoran permanent residence (3 bitcoins), there are currently no prices fixed in bitcoin floating in fiat currencies in the economy.

迄今为止,比特币诞生12年以来,虽然大张旗鼓,但除了萨尔瓦多公民身份(标价3比特币)之外,没有任何一个商品是根据比特币来标价而对于其他法币来说是浮动定价的。

(*)这个是充分说明比特币目前并没有被当做货币用的一个例证,确实如此。

PRINCIPLES FOR A CURRENCY

货币的规律

First, let’s discuss the demonetization of gold. In 1971, the U.S. government terminated the Bretton Woods Agreement, ending the convertibility of the U.S. dollar into gold. Gold stocks were growing too slowly, and, as mentioned earlier, much of it went to jewelry and industry — the most robust theory is that there was not enough gold to keep up with economic growth 10 . Furthermore, there had been long debates over the hampering of monetary policy by sticking to metals, as witnessed by the bullionist controversy 11 .It appears that developed economies have trouble hooking their currencies to a commodity.

首先我们来讨论一下黄金的去货币化过程。在1971年美国政府决定终止布雷顿森林体系,结束了美元与黄金之间的挂钩。黄金的总储备增长太慢了,并且上面也提到了很多黄金流向了珠宝业和工业——目前最完备的理论认为黄金的增长速度是没办法满足经济的增长的 10 。另外,金银本位主义的争论旷日持久 11 。似乎,用一种商品来锚定的办法来发型货币对于发展经济来说是有问题的。

(*)传统的经济学理论认为货币的增长应该要和经济总量的增长保持一个平衡,这样这种货币才有利于经济的发展。黄金本来开采的量就不多,且没法预测,还流向珠宝业和工业(导电性等特质)的话,就会造成通缩。这样用黄金挂钩做货币就显得很糟糕了。但这个在经济学是有争议的,不是金科玉律。

10 Ironically the U.S. deficit caused the dollar to be more widely available and used, in stable supply, by what is called the Triffin paradox

讽刺的是美国其实因为美元被广泛的应用并且稳定供给而遭受了大规模的财政赤字,这个被称之为「特里芬悖论」

(*)特里芬悖论的意思是如果美元和黄金挂钩,而其他货币和美元挂钩(也就是布雷顿森林体系),那么美元取得了核心的地位,别国为了发展国际贸易就必须储备美元,这样美元对于美国而言就是净流出的,美元在海外不断沉淀,则美国必然是逆差过。而美国作为维持美元稳定的主体,又必须是长期顺差国才能保持美元的稳定。这两者都要同时满足是矛盾的。由著名的经济学家罗伯特特里芬提出,所以叫特里芬悖论。

11 Even Ricardo got drawn in, see Ricardo’s 1811-1816 arguments [8],[9], and commentary by Jevons [10].

关于金银本位制的争论,连李嘉图也下场争论过,见1811-1816的争论[文献8][文献9],杰文斯的评论[10]

(*)伯南克也是这个论题里比较出名的经济学家,相关的论文也被引用不少,但塔勒布特看不起伯南克来着,哈哈哈。

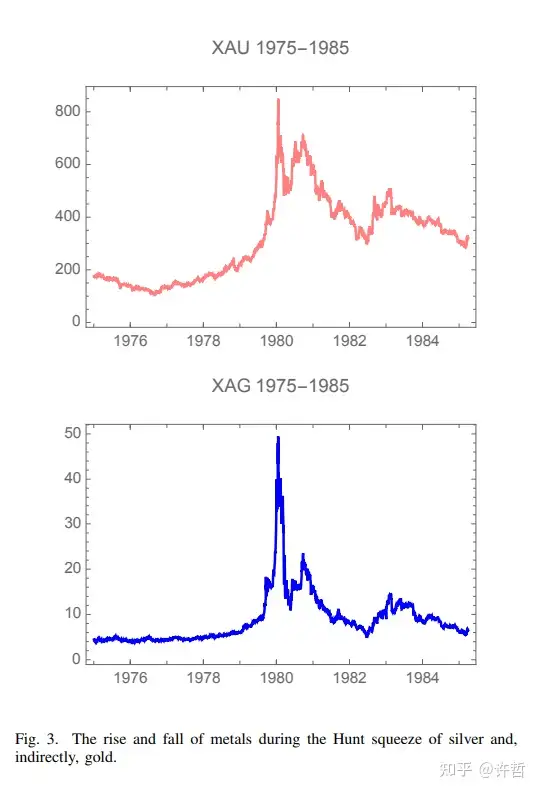

In the early 1970s, the Hunt brothers started to hoard silver (when they started, U.S. citizens were banned from directly owning gold), and accelerated their hoarding in the late 1970s, turning it into a squeeze. It lead to a speculative explosion in the price of silver, as shown in Fig 3, leading by contagion to between a fivefold and tenfold increase in the price of precious metals. Then, upon the deflation of the bubble, metals gave back more than half of their gains and languished for more than two decades. At the time of writing, 41 years later, neither gold nor silver have, inflation adjusted, reached their previous peak. The same effect took place in 2008-2009 in the wake of the banking crisis: gold and silver jumped upwards between 80 and 120 % then subsequently lost most of their gains.

1970年代早期亨特兄弟开始囤白银(那会儿美国公民是不允许私人持有黄金的),且在1970年代末加速囤积了白银,并形成了一次扎空。如上图所显示的那样这导致了白银和黄金的价格发生了投机性的暴涨,并且带动了其他贵金属产生了5到10倍以上的暴涨。然后,随着泡沫的破裂,金属的价格发生了腰斩并且在未来的二十年内萎靡不振。在本文写作的时刻,也就是41年后,经过通胀调整来计算,黄金和白银的价格也没回升到原来的高点。2008-2009年的银行业危机也是同样的模式,黄金和白银的价格在80%到120%之间的幅度飙升然后大部分价值又都还回去了。

Gold and silver proved then that they could neither be a reliable numeraire, nor an inflation hedge. The world had become too sophisticated for precious metals. If we consider the most effective numeraire, it must be the one in which the bulk of salaries are paid, as we will show next.

黄金和白银已经被证明了它们没办法胜任一个好的计价工具,也不是可靠的通胀对冲。这个世界已经变得越来越险恶了。如果我们要考虑使用一种东西作为计价工具,它必须是大部分可以用支付来薪水的,我们接下来看。

Comment 3: Payment system

评论3:支付体系

There is a conflation between “accepting bitcoin for payments” and pricing goods in bitcoin. To “price” in bitcoin, bitcoin the price must be fixed, with a conversion into fiat floating, rather than the reverse

在「接受比特币支付」和用比特币定价之间是有差异的。以比特币计价是值它相对于比特币而言是固定的,并且相对于法币而言它是浮动的,而不是相反。

(*)意思和上面那个萨尔瓦多的公民身份开价3比特币是一个意思。比特币从7万刀左右跌到2万刀,那个公民资格还是卖3BTC,没有变成10.5 BTC保持21万美元的价格才叫以比特币定价,区别于「接受比特币支付」。

Let us go deeper into how a currency can come about. No transaction between two persons is analytically pairwise in an open economy. The root of the confusion lies in the prevalent naïve-libertarian illusion that a transaction between two consenting adults, when devoid of coercion, is effectively just a transaction between two consenting adults and can be isolated and discussed as such 12 . But one must consider the ensemble of transactions and the interactions between agents: people happen to engage in contractual agreements with others; for them a specific transaction is just one piece. To be able to regularly buy goods denominated in bitcoin (whose prices fixed in bitcoin but floating in U.S.$ or some other fiat currency), one must have an income that is fixed in bitcoin. Such an income must come from somewhere, say, an employer. For an employer to pay a salary fixed in bitcoin, she or he must be getting revenues fixed in bitcoin. Furthermore, for the vendor to offer a can of beer in fixed bitcoins, she or he must be paying for the raw material, and have the overhead fixed in bitcoin. The same applies to the mismatch of assets and obligations on a balance sheet. All this requires a parity in bitcoin-USD of low enough volatility to be tolerable and for variations to remain inconsequential.

让我们更深入的来看一看货币是怎么来的。在一个开放的经济体内,没有两个人之间的交易是如同经济学分析里说的那样完美的匹配且成对的出现。这个谎言的根基是来自于普遍的自由主义的臆想:两个独立自由意志的成年人在不受强迫的情况下可以被单独提出来像理论分析那样就能以最高效的形成交易 12 。

现实情况是必须要考虑许许多多交易的整体作用和人和人之间的互动。人们碰巧在一个特定的合同下和人交易,这种情况只是生活中的一隅。如果要以比特币定价的方式来日常性的购买商品(以比特币定价而对美元等法币浮动),那么这个人的收入也应该以比特币来计价。意思是说,这种收入结构意味着一个人的薪水是拿比特币来支付的,他或她比如获得比特币计价的固定收入。并且购买一瓶啤酒也要以比特币计价,他或她支付各类原材料成本和其他开销等等都要以比特币来计价。对于资产负债表的两侧都要以比特币来计价。所有这一切都必须有一个比特币兑美元的足够低波动率的情况下才能忍受,使得这个兑换率的变化不那么灾难性。

(*)这里涉及到的一个概念是「交易成本」。真实世界里的交易不是没成本的,在一个异常孤立的经济学设想里,交易用什么货币清算是无关紧要的,因为可以把所有的交易都附加上一个外汇掉期互换。但真实的世界里,不可能所有涉及到的交易都频繁的做这种附加合同,必须考虑真实世界的日常清算的交易成本。一次涉及到汇率掉期的交易只能是偶尔出现的,不可能日常买菜等琐事里高频出现。

(*)纯粹的用一个个合同来解释自由人的经济活动是一个过度理想化的学术设想而已,是一个真空球形鸡式的构想,真实的世界不是这样的。人们在一个个合同下和人进行理性人博弈互动是偶尔的。大量的日常交易如果有一方要用比特币来进行计价的话,那意味着牵一发而动全身,所有的必须都用比特币来定价。除非比特币和现在最主流的清算方式,也就是美元,其之间的波动率小到可以不产生非常严重的影响。

(*)笔者的生活经验里有接触到一些跨国的不方便用正常银行渠道的清算案例,用USDT的交易远多于BTC。

(*)大体的意思是说比特币倘若真要走货币属性路线,那除非所有人突然都用比特币计价,否则它必须与当下世界的主流清算方式保持一个很小的波动率才有可能。

There are also arbitrage bounds present in any sufficiently efficient economy with relatively free markets. Furthermore, if a vendor prices goods in bitcoin, and the value fluctuates from the initial fixing, the price will be directly or indirectly arbitraged: when the conversion rate to fiat is favorable, customers will buy from the bitcoiner; when it is unfavorable they will either buy elsewhere (indirect arbitrage), or if possible, return previously purchased goods (direct arbitrage). For the price to not be arbitrageable requires the good to be unique and unavailable elsewhere at a price fixed in another currency –in this case it becomes, simply, a proxy for bitcoin. The only items that currently appear to be somewhat priced in bitcoin are other cryptocurrencies, even then not always.

在一个正常的自由市场经济体里中是会有套利边界的存在,如果一个商贩给商品以比特币计价,那么在产生套利机会的时候它就会直接或者间接的套利:当(以比特币计价的商品)换算成法币有利可图时,顾客会从比特币定价者那里买,当换算成法币不划算的时候他们会从其他地方买(非直接套利),或者如果可能的话,还会把之前用比特币买的商品退掉(直接套利)。如果想要价格无法被这样套利,除非一种商品被固定只能用一种货币购买,绑定锁死——这种情况下,这类商品就是比特币的代理。目前来看,比特币唯一绑定购买的商品是其他的加密数字货币,甚至有的还不行。

(*)上面这一段套利的意思是:因为比特币和主流法币的汇率不稳定且自由市场自发的会出现套利行为,所以用比特币固定的去定价日常商品和服务是不可能的。假设一个人用比特币定价一箱啤酒因为比特币波动太大,而套利者一直存在,那么这个商贩平时啥事都别做了,每时每刻都不断修改报价了。

(*)这里的锁定某类商品必须用一种货币清算恰是当今石油-美元体系的方式,即强制用美元清算石油来使得美元的价值始终是存在的,美元成了纸原油,也就是一个代理机制。而比特币作为货币来看的话,唯一用它来购买的只有其他币这是个循环论证了。

(*)当一个货币能且只有它能购买某类大家都需要的商品时,它必然是有价值的。就好比当只有粮票能购买到粮食时,粮票也产生了一种货币属性是可流通的。现在目前全球很多货币的央行的资产负债表里的资产是美元,本身是个二级锚定机制,美元是原油的一级代理,那么这些央行资产表里是美元的货币就是原油的二级代理。

Bimetalism did not last long [11], nor could commodities last as currencies in developed economies[12]. More generally, the reasons multiple currencies exist (in the absence of pegs) is because there is not enough globalization and markets are not entirely free between currency zones. And some goods and services, “such as haircuts and auto repair cannot be traded internationally” [13] ; they are not, to use the language of quantitative finance, arbitrageable.

金银双本位制度并没有持续很久[文献11],商品本位制也没有在发达国家也没持续很久[文献12]。总的来说,目前还有如此多的货币种类存在(在非挂钩货币的情况下),是因为全球化的程度没到那个程度且国家之间的市场也不是彻底全面的开放的。有些商品和服务比如理财或者汽车维修在国际间是非贸易品[文献13];用量化金融术语来说,它们不能被「套利」。

(*)发达国家的理发师和汽车维修师的收入数倍于欠发达国家,并非是因为他们的服务好很多,也并没有引发发达国家的人都集体跑去欠发达国家修车和理发,那是因为存在国界和距离。这也是经济学里说的非可贸易商品的概念。如果所有的商品和服务都在零运费和零关税的情况下可以自由贸易,那么套利会抹平所有的价差。但真实的世界里是不可能这样理想化的。所以才会出现多币种同时存在且没有被套利抹平一切。固定挂钩汇率的情况除外,例如港币挂钩美元,那在经济学意义上,它们名字不一样,但其实是一种货币。

(*)这是补充说明上面那一段套利会让货币互相趋平的一个补丁,按照上面那一段世界就不应该有那么多种货币同时存在了,双币制和单一商品制不成立是好解释了,但无法解释当今世界货币林立。这里给的补丁是真实的世界套利不是那么理想化的。

In 2021, the governments (central and local) share of GDP in Western economies is around 30-60%, one order of magnitude higher than it was in the 1900s. Government employees and contractors get paid in fiat currency; taxes are collected similarly 13

在2021年,西方主要发达经济体的政府(包括中央和地方)占据了GDP大概30%~60%的经济活动总量。这个比1900年代那时候比整整高出了一个数量级。政府雇员和承包商们是以法币形式被支付工资和报酬的,交税也会变得很简单容易 13 。

13The use of the designation “fiat” may be a misleading stretch of language: money is not created by edict but largely via credit, by governments or the private sectors — and both lenders and borrowers need the least volatile currency.

使用「法币」一词来描述在语义上容易产生望文生义的误会;货币并不是由法令来创造出来的而是信用创造出来的。政府或者其他私人部门——借贷双方都需要一个波动比较小的通货。

(*)这里其实主要讲的是货币场景的争夺,倘若真的有一天有一种货币要和法币竞争,那作为货币属性的竞争本质上是在竞争使用场景。也就是要把 ��=�� 右边的用于支付的商品服务的量给提上来。现在政府已经占据了GDP活动的三成到六成了,那么政府只要坚持用法币支付报酬和收税,又有什么东西能和政府法定的法币来竞争呢?用更币圈的话术阐述:政府已经掌握了货币使用场景的51%攻击了。

(*)也不用过于悲观,法币其实并不是政府法令凭空创造的,也是要借其信用做支撑的。津巴布韦政府滥发货币依然是其国家唯一指定的法定货币,但本地已经被弃用了。所谓法币,依然是要用信用支撑的,不是一个敕令就大家所有人都必须认的。

Finally, while within a modern currency zone a bimetallic style dual currency cannot easily exist, the same limitations exist between currency zones; parity between currencies tend to be subjected to volatility bounds. An observation we currency option traders made while doing cross-currency volatility arbitrages is that the volatility of a currency pair is inversely proportional to the trade between the two currency zones — countries heavy into trade such as Hong Kong, Saudi Arabia, the UAE, and Singapore (at some point) have maintained explicit pegs to the U.S. dollar or some basket. There could be an interactive relationship between trade and volatility: one can argue that the stability of a currency-pair (adjusted for the yield curve) encourages trade and trade in turn brings stability to the pair 14 15 .

在一个地区双币制的存在是很难的,相同的情况在两个货币区之间也存在着约束效应;货币之间也存在着波动率的边界。我们汇率期权交易员能明显的观察到的现象是:当我们做跨币种的波动率套利交易的时候汇率的波动率和这两个货币区之间的贸易量存在反比关系。和美国贸易非常密切的地区比如香港,沙特阿拉伯,阿联酋和新加坡(有时候)会出现货币和美元非常挂钩的情况。在汇率的波动率和贸易的密切程度之间会有互动关联的联系。人们可以说货币兑之间的稳定(在收益率曲线平价调整后)促进了贸易,而贸易又反过来促进了货币兑的稳定1415。

(*)这个结论和观察并不意外,我们理解了上文的套利活动的频繁存在就能理解为什么互相贸易比较频繁的两个地区的货币汇率会偏向于稳定了。

(*)期权是一种衍生品,本身是交易一个标的的波动率的,即可以下注它的波动变大和变小。在汇率的期权市场交易就是在交易某两个货币之间汇率变动的波动剧烈程度。所以汇率的期权市场最能直接观察到该汇率兑的稳定性。

(*)这个之间也存在着一种自我加强的正反馈过程,稳定的汇率使得两国之间的贸易并不需要太多考虑汇率波动的风险,而因为不用考虑汇率波动的风险,那么两个之间的贸易会增大而这个增大又加强了汇率的稳定。

14Currency pairs often show fake volatility as the spot price can be fluctuating, but forward contracts do less so, owing to interest rate adjustments in the weak currency: interest rates rise to compensate holders for the devaluation.

货币兑经常出现很多假的高波动,通常出现在现汇市场;不过远期市场很少这样,因为弱势货币的利率调整的关系,利率上升会补偿持有者的贬值。

(*)这里讲的是汇率市场的平价定律,意思是实际货币兑之间的平稳性要比现汇市场的波动率看上去要小。这里并不改变上面通过汇率期权市场观察汇率稳定性的有效性。因为期权定价锚定的也是标的物的未来的价格,汇率期权定价定的外汇远期的波动率而非即期汇率的波动率。所以塔勒布作为汇率期权交易员的观察没问题。

15 .We note here that quantitative finance operates along the lines of neoclassical economic theory in that both share a central principle: absence of arbitrage, which maps to the law of one price — the former, a concept initially aimed at goods and services, may be broadened to include asset valuation [14]. When we apply the law of one price to currencies, we realize using basic arbitrage arguments that the recent globalization does not allow for different currencies to coexist in the same marke: one must win

我们注意到量化金融和新古典主义经济学都遵循的原则:无风险套利不存在假设和一价定律,前者包括了所有的商品和服务,应该囊括资产定价在内[文献14]。当我们应用一价定律在货币上的时候,我们意识到用最基本的套利规则那么当今全球化的请下事实上不允许同一个市场里存在两种不同的货币,有一个必须赢家通吃。

(*)这是另外一个金融学话题,和主旨无关,不展开。

Now bitcoin, as seen in Fig.1 has maintained extremely high volatility throughout its life (between 60% and 100% annualized) and, what is worse, at higher prices, which makes it’s capitalization considerably more volatile, rising in price as shown in Fig. 2 — is it too volatile to fail?

现在再来看比特币的波动率,图1显示比特币在其生命周期里持续产生了超高的波动率(年化大概60%到100%之间)更糟糕的是,其价格越高,使得它的资本化率更加动荡。

(*)总结一下这一整大断的意思:一个东西要成为货币属性的东西,它必须不能和商品的价值之间产生太大的波动率,因为这个世界是存在频繁套利的且普遍遵循一价定律,那么频繁套利会使得改候选货币无法在真实的日常的生活里充当货币的角色,因为交易成本会高到不可忍受(买卖双方要过于频繁的修改交易)。并且这个推论放到国际货币市场上也是完全成立的,能被作为可贸易货币的东西会互相稳定下来,做不到的这不可能成为可贸易货币圈子里的一员。底层的例外是如果你能锚定一种广泛被需要的商品必须用此种货币来交易,但比特币能锚定交易的只有其他币,没有任何一种商品可以。除了萨尔瓦多的公民身份之外一个都没有。货币自由竞争的场景下因为政府活动已经占了GDP的三成到六成,那么在使用场景的竞争上比特币也不可能是法币的对手。

THE DIFFICULTY WITH INFLATION HEDGES

对冲通胀的难题

This does not mean that a cryptocurrency cannot displace fiat –it is indeed desirable to have at least one real currency without a government. But the new currency just needs to be more appealing as a store of value by tracking a weighted basket of goods and services with minimum error.

这并不是说加密数字货币这个形式一定不能取代法币,一个没有政府背景的「真·货币」是一个非常棒的主意。不过这个新的货币需要一个更好的锚定一揽子商品和服务的表现(更小的跟踪误差),让它更能作为价值的存储。

Displacing fiat is not easy, and has been done locally — though no single item has proved to be permanent and the difficulty is best represented in the following example. During the 1970s, the Italian national telephone tokens, the gettoni, were considered acceptable tender, almost always accepted as payment. The price of the espresso when expressed in lira varied over time, but it remained sticky to the gettone. For a while the gettone proved the closest money to track the Fisher Index across 12 communes[15] 16 . And while the gettoni worked for daily purchases such as espresso, it is doubtful that they could have been used as payment for an Alfa Romeo [17].

取代法币不是一个容易的事情,哪怕就是在局部地区而言也是——目前没有一个例子可以证明永久性的法币的替代品。我们现在下面的例子里可以很好的体现出来。在1970年代,意大利国际通话公司发行的token,叫gettoni,被认为是可接受的类货币,几乎都已经是可以用来做日常支付了。以里拉计价的浓咖啡的价格一直在波动,不过以gettoni来定价倒是物价很稳定。一度gettoni被认为 最接近追踪12个社区里的费雪指数的货币。虽然大家都在一段时间里认可gettoni能买到咖啡,不过对于能不能用于买一台阿尔法.罗密欧车表示怀疑。

(*)这里指的不是代金券,比如星巴克发的以人民币计价的礼品券和这里完全是两个概念。这个gettoni 币和里拉没有固定的兑换关系。而它在一定情况下追踪物价要比里拉好,那居民就更乐意拿它做货币使用(买卖双方都希望获得和物价最小的误差方差)。

Considering that communications get cheaper over time, the notion of a telephone call is today, in the Zoom days, obsolete. So the gettone story illustrates the fact that, owing to technological changes, in the long term, no single item, such a telephone call, will permanently track inflation indices and act as a store of value. Even categories have their weights naturally revised over time: the share of food and clothing declined by almost threefold as a proportion of Western consumers expenditure since the great recession.

Thus we can look at an inflation hedge as the analog of a minimum variance numeraire.

考虑到通讯的成本越来越低,在有了Zoom的日子里,打电话的概念都过时了。所以这个gettone 的故事说明了一个事实:由于技术变革,在长期来看,没有一个单独的品类比如电话业服务能长期的追踪通胀指数且作为一个价值存储。哪怕是不断的调整指数里各品类的权重也不行,食物和衣物在消费者中的占比自从大萧条以来已经下降了10倍了。

因此,我们应当把通胀对冲视作是对计价单位的最小方差化。

(*)意思是那家电话公司的积分在一段时间内和物价高度正比相关,但因为通讯业的飞速发展,这个服务大幅贬值。我们很难找到一揽子商品能保持稳定,因为世界是在不断变化的,今天昂贵稀缺的商品和服务明天可能就变得不值钱。要找到一个东西对整体物价保持稳定是不太可能都。

Let us assume that there exists an efficient inflation hedge for period [�0,�] for an index methodology, the one in which the index, constantly revised, is the most stable when it is as a numeraire (adjusting for interest and dividend payments).

让我们假设存在一种有效的通胀对冲,满足在周期[�0,�]内实现一个指数的制定。在这个指数是不断调整,使得它作为一个计价单位最大的稳定化(利率和分红的情况都被考虑在内)

(*)这里数学化了一个理想计价单位的目标,也就是对通胀的完美对冲,一个方差最小的物价跟踪指数。把这个方差最小化的物价跟踪指数做一个ETF的话,就是完美货币了。

Can one find her or his own hedge?

In the parable of the Christ in the temple, Jesus kicked the money changers out of the temple of Jerusalem… Now one wonders why were there were money changers in a place of worship? The answer is that the temple took for currency only the shekel of Tyre, known for its 90% silver content and its ancestral quality control [18] 17 .

Simply, there is a free market for fiat currencies, with the most reliable at the time used by third parties. Before the Euro, there were plenty of currencies in Europe. But long term contracts, investments, and commitments were evaluated in deutschmarks or Swiss francs, sometimes the U.S. dollar; drachmas, liras, and pesetas were there mostly for petty expenditures. So what we had was competition between fiat currencies just as with the shekel-of-Tyre!

This competition provides for a vastly more convenient monetary store of value. For practitioners of quant finance, the most effective inflation hedge can be a combination of bets which includes the short bond.

那人们能找到他或她的完美对冲物吗?

在基督教的典籍里,耶稣把兑换货币的人赶出耶路撒冷的殿……现在有人好奇为什么在一个礼拜的场所里会出现一个兑换货币的人?答案是那个圣殿只收shekel-of-Tyre这一种货币,以90%的银含量和祖传的质量控制而闻名。

很简单的,在法币世界里有一个自由市场会由第三方使用者选出那个时间段里最靠谱的货币。在欧元出现之前,欧洲有许多许多种货币。但长期以来,投资和商业承诺都是以德国马克或者瑞士法郎来约定的,有时候是美元。德拉克马、里拉、比塞塔是最广泛使用的小额支付的工具。所以法币之间的竞争就好比是这个时代的shekel-of-Tyre!

(*)这里的意思是货币自由竞争就解决问题了,不是德国和瑞士的人在做大额的投资协议的时候一样是会选择德国马克或者瑞士法郎。这个是自由竞争选择的结果。

这种竞争提供了一种方便得多的货币价值储存方式。对于量化金融的参与者来说,最有效的通胀对冲可以包含一系列的头寸组合包括一些短期债券。

(*)这里的意思是要创造出一种完美的通胀对冲物使得物价方差最小化是不太现实的,让自由市场发挥作用,让法币们卷起来就可以了。如果懂量化金融,什么短期债券之类的组合大家都可以比赛去追踪最好的通胀对冲,量化金融师们也卷起来。

SOME ADDITIONAL FALLACIES

其他一些谬论

1) Fallacy of libertarianism: The belief that bitcoin is an offshoot of libertarian and Austrian economics has no solid backing — it has the same lack of rigor as the one behind the belief that cryptos represent a “hedge for inflation”. Spitznagel [19] had already, in 2017, debunked the notion that bitcoin can be a safe haven (as discussed next) or that the principles of Austrian economics can be invoked in support of cryptocurrencies.

1)对于比特币是自由主义和奥地利学派的分支是完全没有支撑的看法——就好像那些相信加密数字货币能对冲通胀一样不严谨。Spitznagel [文献19]在2017年已经揭穿了比特币是避险天堂的谎言(下文会讨论),也证伪了加密数字货币是被奥地利学派支持的看法。

Comment 4: Law vs. Regulations vs. Rules

评论4:法律VS监管VS规则

Libertarianism is about the rule of law in place of the rule of regulation. It is not about the rule of rules.

Libertarianism is fundamentally about the rule of law in place of the rule of regulation. It is not about the rule of rules — mechanistic, automated rules with irreversible outcomes. The real world is fraught with ambiguities and even Napoleonic law (far less mechanistic than crypto rules) cannot keep up — to wit, as a risk management directive, most commercial contracts traditionally prefer forums of dispute resolution to be under the more flexible Anglo Saxon common law (London, NY, Hong Kong) that rules on balance, intent, and symmetry in contracts. This applies of course to quantitative finance products such as complex derivatives contracts for which one needs to minimize the legal risk. Nor is libertarianism about total distrust.

自由主义的基础是用法律来取代监管,而不是用规则来统治——机械的自动化的规则并且产生不可逆转的结果。真实的世界上充斥着模糊性的,哪怕类似拿破仑法典(远没有加密货币机制那么机械)也不能完全跟上。在风险管理大部分合同都是根据普通法的原则(伦敦,纽约,香港)来裁定的。在量化金融领域,诸如复杂的金融衍生品合约双方当让希望最小化法律风险。

2) Fallacy of safe haven, I (protection for financial tail risk): The experience of March 2020, during the market panic upon the onset of the pandemic, when bitcoin dropped farther than the stock market —and subsequently recovered with it upon the massive injection of liquidity is sufficient evidence that it cannot remotely be used as a tail hedge against systemic risk. Furthermore, bitcoin appears to respond to liquidity, exactly like other bubble items. It is also uncertain what could happen should the internet experience a general, or an even a regional, outage — particularly if it takes place during a financial collapse.

2)关于避险天堂的谎言 I(对于尾部风险的保护):从2020年3月的经验来看,当市场陷入恐慌的时候,比特币跌的甚至比股市还要多——以及随后在大规模注入流动性后的复苏,足以证明它根本不能被用作尾部对冲系统性风险。并且,比特币表现出的性质是对流动性的正比反应,就和其他泡沫资产是一模一样的。很难想象当互联网出现大问题的时候,甚至是区域性质的大停电会不会出现大问题——尤其是这个时候恰好发生金融危机。

3) Fallacy of safe haven, II (protection from tyrannical regimes): To many paranoid antigovernment individuals and of others distrustful of institutions, bitcoin has been marketed as a safe haven — also with an open invitation to fall for the fallacy that a volatile electronic token in a public setting is a place for your hidden treasure.

By its very nature, bitcoin is open for all to see. The belief in one’s ability to hide one’s assets from the government with a public blockchain easily triangularizable at endpoints, and not just read by the FBI but also by people in their living rooms, requires a certain lack of financial seasoning and statistical understanding — perhaps even a lack of minimal common sense. For instance a Wolfram Research specialist was able to statistically detect and triangularize “anonymous” ransom payments made by Colonial Pipeline on May 8 in 2021 [20] — and it did not take long for the FBI to restore the funds.

3)关于避险天堂的谎言 II(对抗专制暴政):太多过于敏感的反政府主义者和不信任机构的人表示比特币是一个安全的避险天堂,它能帮你隐匿你的财产。

不过就其性质而言,比特币对所有人都是开放的。就政府层面而言其实用技术手段很容易找到一个人,不用FBI出手,所有人在自己家客厅里就可以做到,只需要一些财务和统计学上的知识。举个例子,Wolfram 的一个研究员就能用统计学的办法来把2021年5月8日的赎金的幕后匿名者给抓出来。FBI去追还失款都没用多久。

We can safely assume that government structures and computational power will remain stronger than those of distributed operators who, while distrusting one another, can fall prey to simple hoaxes.

In the cyber world, connections are with people one has never met in real life; infiltration by government agents has proven to be extremely easy18. By comparison, the mafia required a Sicilian lineage for “friends of ours” for security clearance. One never knows the degree of governmental surveillance and its real capabilities.

The slogan “Escape government tyranny hence bitcoin” is similar to advertisements in the 1960s extolling the health benefits of cigarettes.

我们可以有把握地认为,政府结构和计算能力仍将强于那些相互不信任的分布式运营商。在网络世界里,网上的人们互相其实在现实生活里互相都不认识,政府要渗透可太容易了。相比之下,黑帮要求西西里血统来作为自己人的安全保障。人们永远不知道政府监控的程度及其真正的能力。

「逃离政府暴政,比特币应运而生」的口号就好比1960年的吹捧香烟有益健康的广告。

4) Fallacy of the Agency problem: One might have the impression that, by being distributed, Bitcoin would be democratic and reduce the agency problem perceived to be present among civil servants and bankers. Unfortunately, there appears to be a worse agency problem: a concentration of insiders hoarding what they think will be the world currency, so others would have to go to them later on for supply. They would be cumulatively earning trillions, with many billionaire “Hodlers” — in comparison the “evil civil servants” behind fiat money make, at best, lower middle class wages. This situation represents a wealth transfer to the cartel of early bitcoin accumulators.

4)解决代理人问题的谎言:有人可能听闻过因为去中心化,比特币的世界是更民主公平的且能解决公务员和银行家带来的代理人问题。不过很不幸,现实是比特币世界的代理人问题更严重。一群内部人士集中在囤积他们认为将成为世界货币的东西,所以其他人以后必须去他们那里获取供应。他们能逐渐赚万亿,并且有许多十亿身家的「持币人」,相比之下玩儿的公务员只赚取了比较中等的工资。这种情况代表着财富向早期比特币积累者的卡特尔模式转移。

CONCLUSION

结论

We have presented the attributes of the blockchain in general and bitcoin in particular. Few assets in financial history have been more fragile than bitcoin.

我们已经介绍了区块链的一般属性和比特币的具体属性。在金融历史上,很少有资产比比特币更脆弱。

The customary standard argument is that “bitcoin has its flaws but we are getting a great technology; we will do wonders with the blockchain”. No, there is no evidence that we are getting a great technology — unless “great technology” doesn’t mean “useful”. And at the time of writing —in spite of all the fanfare — we have done still close to nothing with the blockchain.

通常的标准论点是「比特币虽然有很大的缺陷但它依然是一个伟大的技术创新,我们会期待区块链技术发挥作用」。不,现在没有任何证据表明区块链技术是一项伟大的技术创新——除非伟大的技术创新不意味着有用。并且在写作的当下,尽管大肆吹捧我们始终没有找到区块链的任何真实应用。

So we close with a Damascus joke. One vendor was selling the exact same variety of cucumbers at two different prices. “Why is this one twice the price?”, the merchant was asked. “They came on higher quality mules” was the answer.

We only judge a technology by how it solves problems, not by what technological attributes it has.

我们用一个大马士革的笑话来结束。一个小贩以两种不同的价格卖着完全相同的黄瓜。「为什么它们的价格不一样?」一个商人问道。答案是:「因为那个贵的是用更贵的驴运过来的」。

我们只以解决了什么问题来判断一个技术的价值,不是以技术性质来判定的。

REFERENCES

[1] S. Nakamoto, “Bitcoin: A peer-to-peer electronic cash system,” Tech. Rep., 2008.

[2] J. Von Neumann, “Various techniques used in connection with random digits,” Appl. Math Ser, vol. 12, no. 36-38, p. 3, 1951.

[3] A. Narayanan and J. Clark, “Bitcoin’s academic pedigree,” Communications of the ACM, vol. 60, no. 12, pp. 36–45, 2017.

[4] O. J. Blanchard and M. W. Watson, “Bubbles, rational expectations and financial markets,” NBER working paper, no. w0945, 1982.

[5] M. K. Brunnermeier, “Bubbles,” in Banking Crises. Springer, 2016, pp. 28–36.

[6] D. Graeber, Debt: The first 5000 years. Penguin UK, 2012.

[7] N. N. Taleb, Antifragile: things that gain from disorder. Random House and Penguin, 2012.

[8] D. Ricardo, Reply to Mr. Bosanquet’s practical observations on the report of the Bullion Committee. J. Murray, 1811, vol. 10.

[9] ——, Proposals for an economical and secure currency, 1816.

[10] W. S. Jevons, A Serious Fall in the Value of Gold Ascertained: And Its Social Effects Set Forth. E. Stanford, 1863.

[11] F. R. Velde and W. E. Weber, “A model of bimetallism,” Journal of Political Economy, vol. 108, no. 6, pp. 1210–1234, 2000.

[12] T. J. Sargent and M. Wallace, “A model of commodity money,” Journal of Monetary Economics, vol. 12, no. 1, pp. 163–187, 1983.

[13] P. Krugman, M. Obstfeld, and M. Melitz, “International economics: Theory and policy,” 2017.

[14] S. A. Ross, Neoclassical finance. Princeton University Press, 2009, vol. 4.

[15] L. Campiglio, “Un’analisi comparata del sistema dei prezzi nei venti comuni capoluogo di regione,” Rivista Internazionale di Scienze Sociali, vol. 94, no. 3, pp. 329–377, 1986.

[16] M. Nair and R. Emozozo, “Electronic currency in africa: M-pesa as private inside money,” Economic Affairs, vol. 38, no. 2, pp. 197–206, 2018.

[17] K. Colucci and C. Moiso, “Il fenomeno delle monete virtuali: opportunità per telecom italia,” Notiziaro Tecnico /Telecom Italia, vol. 1, pp. 76–89, 2014.

[18] J. Murphy-O’Connor, “Jesus and the money changers (mark 11: 15-17; john 2: 13-17),” Revue Biblique (1946-), pp. 42–55, 2000.

[19] M. W. Spitznagel, “Why cryptocurrencies will never be safe havens,” Von Mises Institute, 2017. [20] D. Porechna, “Darkside update: The fbi hacks the hackers?” Wolfram Research, June 2021.

(*)我肝太晚了,读后感以后再写,感兴趣的关注追更。